What Is RippleNet? Understanding Its Impact on Global Payments, Blockchain, and Financial Systems

What Is RippleNet?

Picture this: you’re sending money from Japan to Brazil. A standard bank wire takes 3 to 5 business days, passes through two or three correspondent banks along the way, and each one takes a cut. By the time the money arrives, the recipient gets less than you sent — and neither of you knows exactly when it will land. RippleNet offers a different approach. The same transfer completes in seconds, with a fixed fee and full visibility at every step. That’s not a marketing pitch — it’s what the technology actually does, and why more than 300 financial institutions across 55+ countries have connected to the ripple payment network.

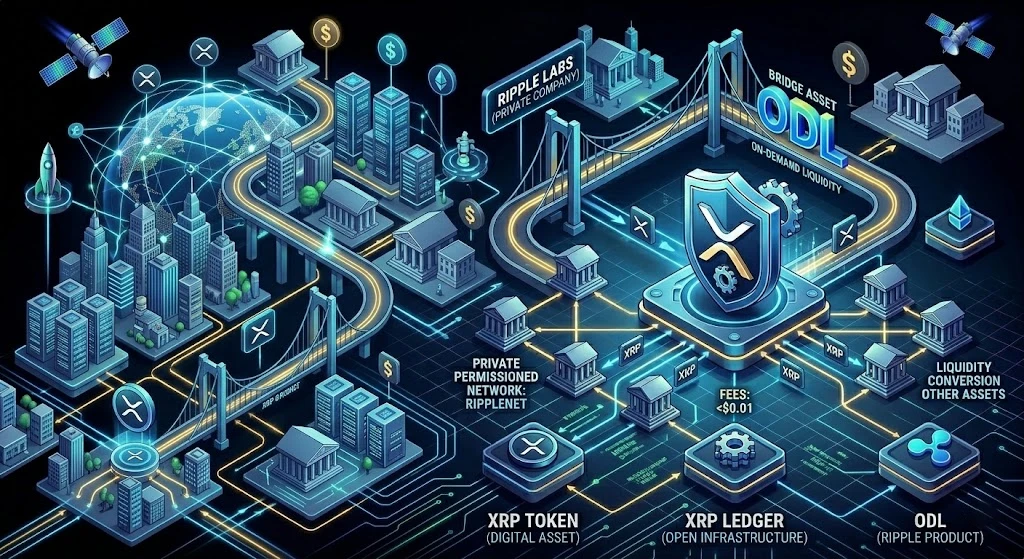

So what is RippleNet, exactly? RippleNet is a global payments network built by Ripple Labs that connects banks, payment providers, and financial institutions, allowing them to send money directly to each other — without the long chain of intermediaries that makes traditional cross-border payments slow and expensive.

One thing worth clarifying upfront: RippleNet is not the same as XRP. This is one of the most common sources of confusion, and we’ll cover it properly in a separate section.

How the Ripple Payment Network Works

Cross-Border Payments

The traditional international payment system runs on correspondent banking. Bank A doesn’t have a direct relationship with Bank B in another country, so they both hold accounts at an intermediary Bank C — sometimes Bank D as well. Every intermediary charges a fee, holds the funds for a period, and adds uncertainty to the timeline.

According to McKinsey research, the average cost of an international transfer runs around 6% of the amount sent. For transfers to developing countries, the figure is even higher. That’s money sitting in intermediaries’ pockets rather than reaching recipients.

RippleNet changes this model. Member institutions — banks and payment operators — connect to a shared infrastructure and can transfer funds to each other directly, bypassing the correspondent chain. A transaction confirms in 3 to 5 seconds. The fee is locked in before the transfer is initiated. The status is visible throughout the process.

The key difference from the traditional system is pre-confirmation. The sender sees the exact amount the recipient will receive before pressing send. No surprises on the other end.

Financial Institution Integration

Connecting to RippleNet isn’t like installing an app. Banks integrate Ripple’s APIs into their existing systems, adopt data exchange standards, and go through a verification process. In return, they gain access to the full network of connected institutions.

There are three core products through which banks work with Ripple:

- xCurrent — a messaging and settlement system for real-time interbank transactions. Does not require XRP.

- ODL (On-Demand Liquidity, formerly xRapid) — uses XRP as a bridge asset to provide instant liquidity in the destination currency without pre-funded accounts.

- xVia — a standard interface for sending payments through the Ripple network with attached transaction data.

Most banks start with xCurrent. It’s simpler to integrate and doesn’t require working with cryptocurrency. ODL is the choice for institutions that want to eliminate the need to hold pre-funded reserves in foreign currencies altogether.

Settlement Process

How does an actual payment move through RippleNet? Stripped down to the essentials, it works like this.

The sending bank initiates the transfer through the Ripple interface. The system instantly checks liquidity and calculates the optimal route. If ODL is being used, XRP is automatically purchased on an exchange, converted into the target currency on the receiving side, and sold — the whole sequence happens in seconds. The receiving bank records the credit in its own system. Every step is logged on the XRP Ledger.

The atomic settlement design means the transfer either completes fully or doesn’t happen at all. There’s no scenario where money leaves one account but fails to arrive at another.

What Is XRP and How It Relates to RippleNet

XRP Token Overview

XRP is a digital asset created by Ripple Labs. It lives on the XRP Ledger — a decentralized blockchain that operates independently from Ripple the company. Transaction confirmation takes 3 to 5 seconds. Fees run a fraction of a cent. The total supply is capped at 100 billion tokens, most of which are already in circulation or locked in Ripple’s escrow accounts.

By market capitalization, XRP consistently ranks in the top ten cryptocurrencies. Its design is different from Bitcoin or Ethereum: XRP wasn’t built for mining or smart contracts. It was built specifically for payment settlement.

XRP vs Ripple (Key Difference)

Here’s where the confusion usually starts. Ripple is a private company. XRP is a token that exists on an open blockchain. Ripple Labs created XRP, holds a significant portion of the supply, and uses it in its products — but it does not legally control the token itself or the XRP Ledger.

An analogy that works: Toyota built the car, but Toyota doesn’t own the roads it drives on. Similarly, Ripple Labs created XRP, but the XRP Ledger is open infrastructure governed by a network of independent validators.

This distinction matters beyond theory. In 2020, the SEC filed a lawsuit against Ripple Labs, claiming the company had conducted unregistered securities sales — meaning sales of XRP. The case reached a resolution in 2023 and 2024, with a partial win for Ripple: the court ruled that XRP sales to retail investors on exchanges do not constitute securities transactions, though institutional sales fall under a different standard.

Role of XRP in Payments

Why does XRP exist at all if banks can use RippleNet without it? The answer is liquidity.

When a bank wants to send, say, Mexican pesos to Nigerian naira, it needs liquidity in both currencies. The traditional solution is correspondent accounts — the bank holds reserves in dozens of currencies around the world. That’s expensive and capital-intensive.

ODL solves this differently. XRP acts as the bridge: the bank converts pesos into XRP, transfers XRP to the destination market in seconds, and XRP is converted there into naira. The bank never needs to hold pre-funded reserves in non-major currency pairs.

RippleNet vs XRP

Short version:

- RippleNet — payment infrastructure for banks and financial institutions. Can be used without XRP.

- XRP — a digital asset for providing instant liquidity. Exists independently of RippleNet.

- ODL — Ripple’s product that combines both: uses RippleNet for data transmission and XRP for value transfer.

Think of it like rail infrastructure versus the cargo. The railway (RippleNet) can carry freight in different types of cars. XRP is one type of car — the fastest and cheapest option — but not the only one available.

Ripple Payment Protocol Explained

The technical foundation of RippleNet is RTXP — the Ripple Transaction Protocol. It’s a set of rules and standards that govern how network participants exchange payment messages.

One of its core features is atomic settlement. A transfer either completes entirely or fails entirely. There’s no partial state where money is in transit between accounts with no clear ownership.

Another feature is built-in FX support. The protocol lets you specify the currency being sent and the currency in which it should arrive, then finds the optimal conversion path automatically.

Ripple has also integrated with ISO 20022 — the international messaging standard that most major global payment systems, including SWIFT, adopted by 2025. This lowers the technical barrier for banks that already operate under this standard to connect to RippleNet.

Advantages of RippleNet

Why would a bank actually consider switching from the established correspondent system? The numbers make the case.

- Standard international wire: 1 to 5 business days. RippleNet transaction: 3 to 5 seconds.

- Ripple’s own data shows ODL reduces transaction costs by 40 to 70% compared to traditional correspondent banking, primarily by eliminating the need for pre-funded accounts.

- Payment status is visible at every stage. The sender knows the exact amount that will arrive before initiating the transfer.

- Liquidity access. ODL enables transactions in low-liquidity currency corridors without holding standing reserves.

- Network scale. 300+ financial institutions across 55+ countries — this is live infrastructure, not a pilot program.

There are limitations too. RippleNet is a permissioned network: institutions go through verification before connecting. It’s not as open as the Bitcoin network. For some participants, that’s an advantage — regulatory compliance, controlled access. For others, it’s a constraint.

Real-World Use Cases of RippleNet

Abstract advantages are one thing. Here’s what it looks like in practice.

SBI Remit in Japan uses ODL for transfers between Japan and the Philippines. This is one of the world’s largest remittance corridors — millions of Filipino workers in Japan send money home regularly. Before RippleNet, transfers took days. Now they take minutes.

Tranglo in Southeast Asia is a major payment operator using ODL for regional transfers. The company processes millions of transactions per month through Ripple’s infrastructure.

Banco Rendimento in Brazil integrated RippleNet for processing corporate international payments. Companies making frequent large cross-border transfers now have a more predictable and cheaper tool than the traditional banking route.

Sentbe in South Korea connected ODL for transfers from Korea to Southeast Asia. According to the company, processing speed increased and operational costs dropped.

These aren’t pilots. They’re production systems with real transaction volumes.

Future of RippleNet and XRP

A few directions worth watching.

First, CBDCs. Central banks worldwide are actively exploring digital currencies. Ripple is already involved in several pilot projects — including with the central banks of Palau, Bhutan, and Montenegro. The XRP Ledger could become the settlement infrastructure for cross-border CBDC transactions. That’s a potentially enormous market.

Second, asset tokenization. The XRP Ledger supports token issuance, and Ripple is actively positioning the blockchain for tokenizing real-world assets — bonds, real estate, trade finance. In 2024, Ripple launched its own dollar-pegged stablecoin, RLUSD.

Third, regulatory clarity in the US. The partial resolution of the SEC lawsuit opens the door for Ripple to operate more actively in the American market — which, until now, it approached with significant caution. The US is a major international payments market.

Competition hasn’t disappeared. SWIFT launched GPI and adopted ISO 20022. Stellar — founded by one of Ripple’s co-founders — offers similar solutions. New blockchain platforms are staking claims to the same market. But Ripple enters any competitive scenario with a live network and real institutional partners. That’s a meaningful head start.

Key Takeaways

- RippleNet is a payments network for banks and financial institutions that enables cross-border transfers in seconds rather than days, at lower cost and with full transaction transparency.

- XRP and RippleNet are separate things. RippleNet works without XRP. ODL uses XRP as a bridge asset to provide instant liquidity without pre-funded foreign currency reserves.

- More than 300 financial organizations in 55+ countries use Ripple’s infrastructure for live payment operations — not test environments.

- ODL reduces transaction costs by 40 to 70% versus traditional correspondent banking, by eliminating the need to hold standing reserves in foreign currencies.

- Growth directions include CBDC settlement infrastructure, real-world asset tokenization, and expanded US market access following the partial resolution of the SEC case.

Expert Insight

According to Gemini’s Cryptopedia: “RippleNet is a network of banks, payment providers, and other financial institutions that use Ripple’s technology solutions to conduct transactions more efficiently. The network uses blockchain technology to enable fast, reliable, and cost-effective international payments.”

That description captures the mechanics accurately, but leaves out one important detail: RippleNet is a permissioned network for verified financial participants, not an open blockchain. That’s precisely what makes it attractive to banks that need both speed and regulatory compliance — and what distinguishes it from most crypto projects, where openness and decentralization come first.

Conclusion

International payments are one of the most conservative corners of finance. The correspondent banking system took decades to build, and banks don’t abandon it lightly. Despite that, RippleNet managed to bring more than 300 financial institutions on board over ten years.

Not because it’s blockchain — most banks don’t particularly care about that. But because it’s faster, cheaper, and more transparent. Three arguments that make sense to any CFO without any crypto knowledge required.

Will RippleNet dominate international payments in ten years? Hard to say. Competition is real, the regulatory landscape keeps shifting, and SWIFT isn’t backing down. But Ripple’s current position — live network, institutional partners, regulatory progress — puts it among the strongest contenders for that market.

FAQ

What is RippleNet?

RippleNet is a global payments network built by Ripple Labs that connects banks, payment providers, and financial institutions for real-time international transfers. Transactions settle in 3 to 5 seconds with a fixed fee and full visibility at every stage. More than 300 organizations across 55+ countries are currently connected to the network.

How is RippleNet different from XRP?

RippleNet is payment infrastructure for financial institutions. XRP is a digital token that exists on the independently operated XRP Ledger blockchain. Banks can use RippleNet without XRP, through the xCurrent product. XRP comes into play through ODL — for cases where instant liquidity in a foreign currency is needed without pre-funded correspondent accounts.

What is ODL in finance?

ODL stands for On-Demand Liquidity. It’s a Ripple product that uses XRP as a bridge asset: funds are converted into XRP, transferred to the target market in seconds, and converted there into the local currency. The whole process takes seconds. The main benefit is that banks don’t need to hold standing reserves in dozens of foreign currencies.

Can RippleNet be used without XRP?

Yes. The xCurrent product lets banks exchange payment messages and settle transactions through RippleNet without using XRP. Most banks start here — it’s simpler to integrate and doesn’t require working with cryptocurrency. XRP is only involved through ODL.

Is Ripple centralized or decentralized?

RippleNet is a centralized payment network: participants go through verification, and Ripple Labs manages the product. The XRP Ledger — where the XRP token lives — is a decentralized blockchain governed by a network of independent validators. These are two different things that often get conflated.

Published Articles

Popular

PopularBitcoin Pizza Guy: The Story Behind the First Real Bitcoin Purchase

Introduction The history of Bitcoin is full of dramatic ups and downs,...

Popular

PopularThe Meme Economy: How Internet Humor Shapes Culture, Markets, and Crypto

Introduction Ten years ago, the idea that a picture of a dog...

Popular

PopularWhat is the Omniverse? Exploring the Ultimate Multiversal Concept

Introduction Do you know what the omniverse is? Is this concept real?...

Bitcoin Taproot Explained: What the Upgrade Means for BTC

Introduction Unfortunately, the most popular cryptocurrency today – Bitcoin – was not...

Crypto On-Ramps and Off-Ramps Explained: How Fiat and Crypto Move In and Out

Entering the world of digital assets often feels like trying to cross...

Crypto Basics Explained: A Beginner’s Guide to Cryptocurrency and Trading

Introduction The world of finance is changing right before our eyes. Just...